My stated intent with this blog is to help my fellow Boomers navigate through the morass of issues that are facing those of us born between 1946 and 1964 as we age together. I think I know what those major issues are; at least I know which ones keep me awake at night. In the interest of democracy and the realization that there are most probably many, many other issues facing Boomers that I have not yet encountered I tried a little experiment: I GOOGLED “problems facing Boomers” and, in 1/3 of a second I received 565,000 responses. Five Hundred and Sixty Five Thousand! It’s no wonder I have a hard time getting the recommended amount of sleep every night.

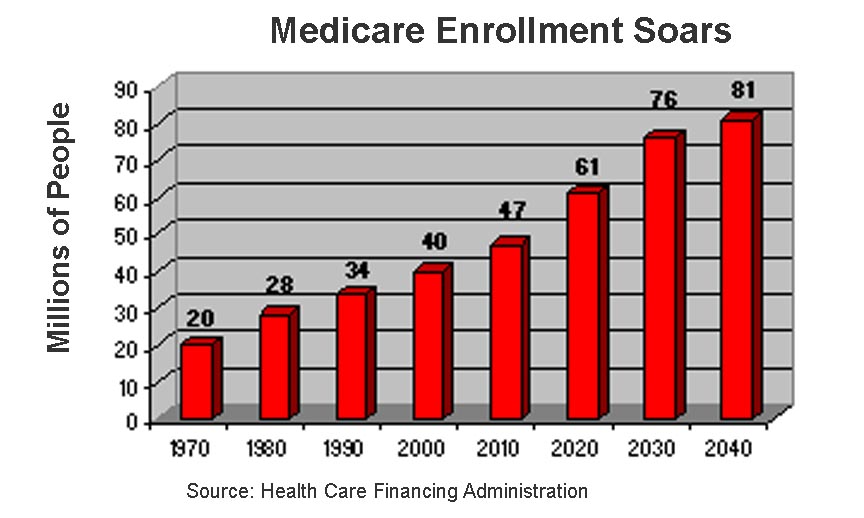

The first thing that jumped out at me was a FOX NEWS report from last year that simply stated “If  rates of disease and disability continue at their current levels, America will become a nation of sick, senile, disenfranchised, impoverished seniors, with too few resources to care for them and astronomical medical costs that will cripple our economy.” Cheery thought, that, but it kind of sums up challenge. I don’t know about you but I am not looking forward to living out my golden years as a depressed, sickly old man wearing tattered Dockers and an old flannel shirt waiting on the veranda of my government subsidized housing for one of my grandchildren to pick me up for an outing to the local park, hoping I can remember his or her name when they arrive. So, I suppose Health and Healthcare that is affordable needs to be at the top of the list of every Baby Boomer’s worry lineup.

rates of disease and disability continue at their current levels, America will become a nation of sick, senile, disenfranchised, impoverished seniors, with too few resources to care for them and astronomical medical costs that will cripple our economy.” Cheery thought, that, but it kind of sums up challenge. I don’t know about you but I am not looking forward to living out my golden years as a depressed, sickly old man wearing tattered Dockers and an old flannel shirt waiting on the veranda of my government subsidized housing for one of my grandchildren to pick me up for an outing to the local park, hoping I can remember his or her name when they arrive. So, I suppose Health and Healthcare that is affordable needs to be at the top of the list of every Baby Boomer’s worry lineup.

Then, it seems, all the concerns about Money and Inflation combined with anticipated Longevity for Boomer’s in general. In simple terms, the Fear of Outliving Assets commands a high place on every Boomer’s list. How to know when enough is enough, that’s the rub. Assuming you think you have “enough” when its time to cut back and try to enjoy whatever is left of your days with our Federal Budget Deficit running in excess of $1 Trillion per year with no end in sight and accumulated debt at $16.5 Trillion and growing is frightening to say the least. It seems we are being led to believe that allowing the Federal Government to keep minting money at breakneck speed is a good thing for our economy. The believe that somehow we will spend our way out of our national fiscal problems flies in the face of all lessons economic I learned over the last 60 years. The simple concept that was taught that when there is more and more currency in the system chasing a finite amount of goods and services the effect squirts out as inflation seems to have been lost in the current environment. Thinking about a day when you might take that last distribution from an IRA account because your money ain’t worth what it used to be and it cost a lot more to live to that point than you ever thought possible and you are left with nothing but a meager monthly distribution from Social Security to support yourself and your spouse that is younger and much healthier than you – now that’s the stuff of which nightmares are made.

Another worrisome issue that jumped out at me, one I had not considered on my own because I have a committed and caring spouse, are the unique challenges facing Single Baby Boomers as they age. I was somewhat taken aback to read that 1 in 3 of the almost 80 Million Boomers is either divorced or never-married or widowed and of that population of more than 25 Million Americans only 10% fall into the widowed category. Among the commonalities of this growing segment is that they tend to be younger, female and non-white. As a group, they become disabled at almost twice the rate of married couples and are less likely to have adequate health insurance. The obvious concerns of who will care for them if they do become incapable on their own are exacerbated by the economic challenges of living alone.

Many Boomer’s are part of what is known as the “Sandwich Generation“; simultaneously having to care for family members that are both older and younger. I think we all know Boomers that have been ensnared in that web with a living parent that needs a significant amount of care and children that have either never left the nest or have returned as victims of the challenging economy or other social problems. The tax of the energy and resources on our contemporaries that are caught as the meat in the middle of this sandwich can be overwhelming.

Functional Decline is another concern of Boomers that I personally hadn’t spent much time thinking about, although I find it distressing that what I once thought of as my razor-sharp memory needs ever more reliance upon a digital calendar for prompts about the normal and necessary parts of day-to-day living.

Abuse, Neglect and Financial Exploitation have their own places up and down the roster of those things about which to be concerned. I have a friend that is an attorney specializing in Elder Law. Apparently, the need for this specialty is growing exponentially.

Death and Dying mixed up with cultural and religious beliefs creates its own menu of concerns for Boomers who want to have a say in how their own lives end. How and when to make their wishes known to family members and the worries about whether those wishes will be honored are among the details that must be reconciled.

Where To Live is another challenge facing Boomers. Layering the desires to be close to (or not) other family members, health care facilities, recreational opportunities, entertainment, shopping and religious facilities with the need or willingness to move from an existing home creates another set of insecurities.

My goal over the coming period of time is to explore these issues in-depth and other concerns that are brought to my attention with a focus on how best to attack each of the challenges as we age together. If there is something keeping you awake at night that you would like to have me address please let me know.